Sterling spikes often begin quietly until a number hits the tape. Then price gaps, spreads widen, and momentum accelerates. For GBP traders, CPI and PMI releases are the most frequent catalysts of sharp intraday spikes. These prints don’t just move charts; they reset the market’s path for Bank of England policy, reprice yields, and re-order positioning across GBP pairs. Here’s how to decode the moves and trade these Sterling spikes with discipline.

Why CPI Matters Most

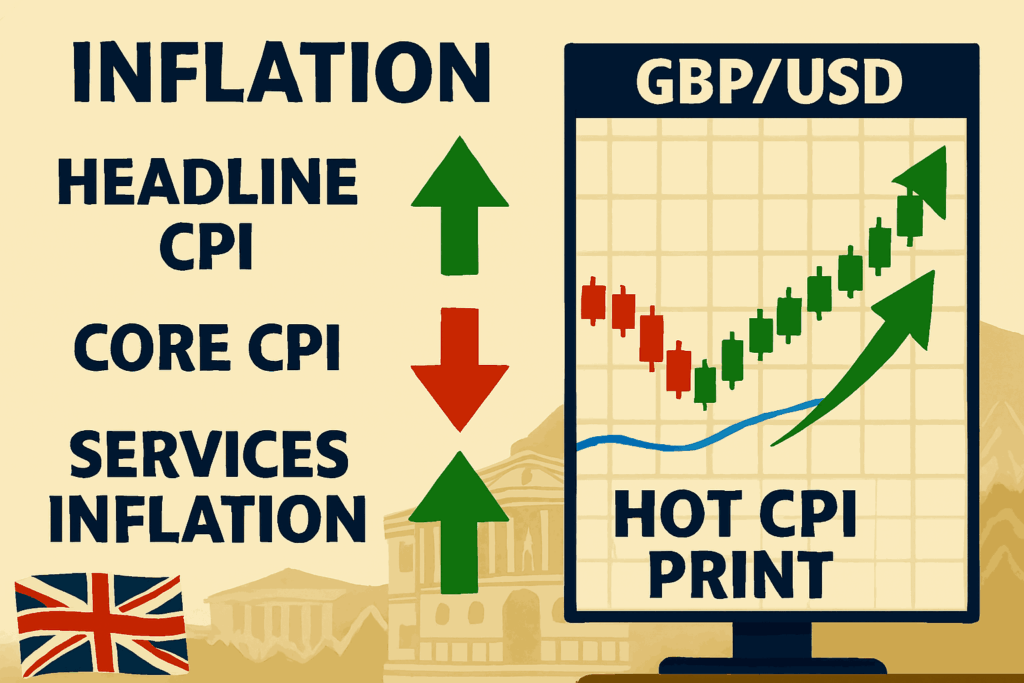

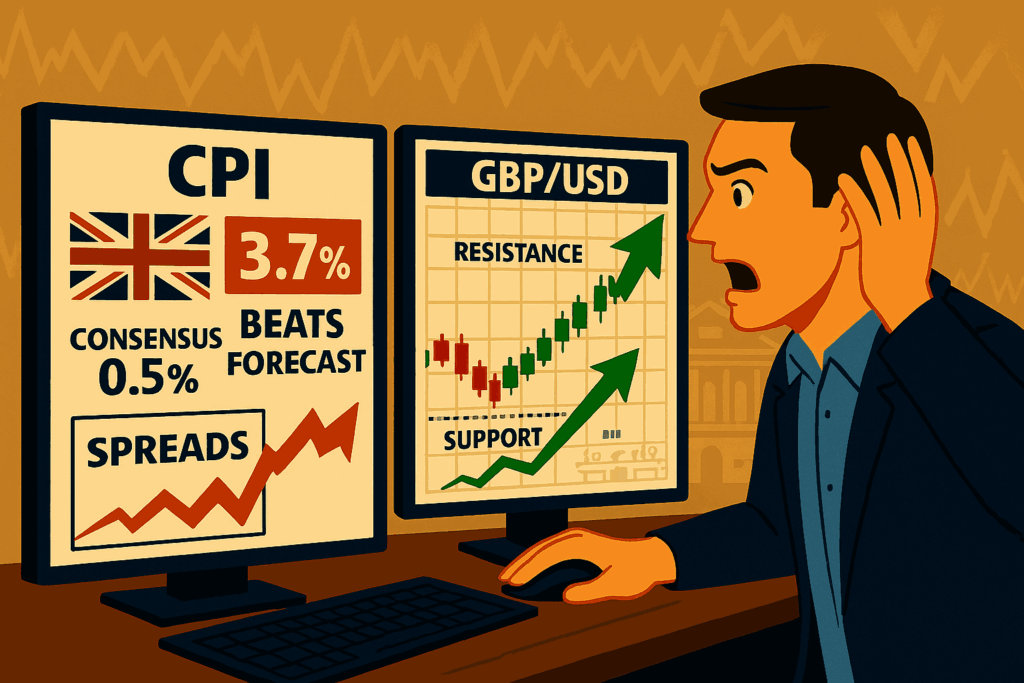

UK CPI directly informs BoE policy. A hot CPI (headline or core above consensus) pushes rate expectations higher, lifting GBP especially against low-yielders (EUR, CHF, JPY). A soft CPI does the opposite. Beyond the headline:

- Core CPI (ex-food & energy) shows underlying inflation pressure key for policy trajectory.

- Services inflation is closely watched because it’s sticky and wage-sensitive.

- Month-on-month vs year-on-year: MoM surprises can spark fast intraday reactions; YoY trends anchor the bigger narrative.

Trading note: Markets move on the delta vs consensus. If CPI matches forecasts, reaction is often muted even if the level is high.

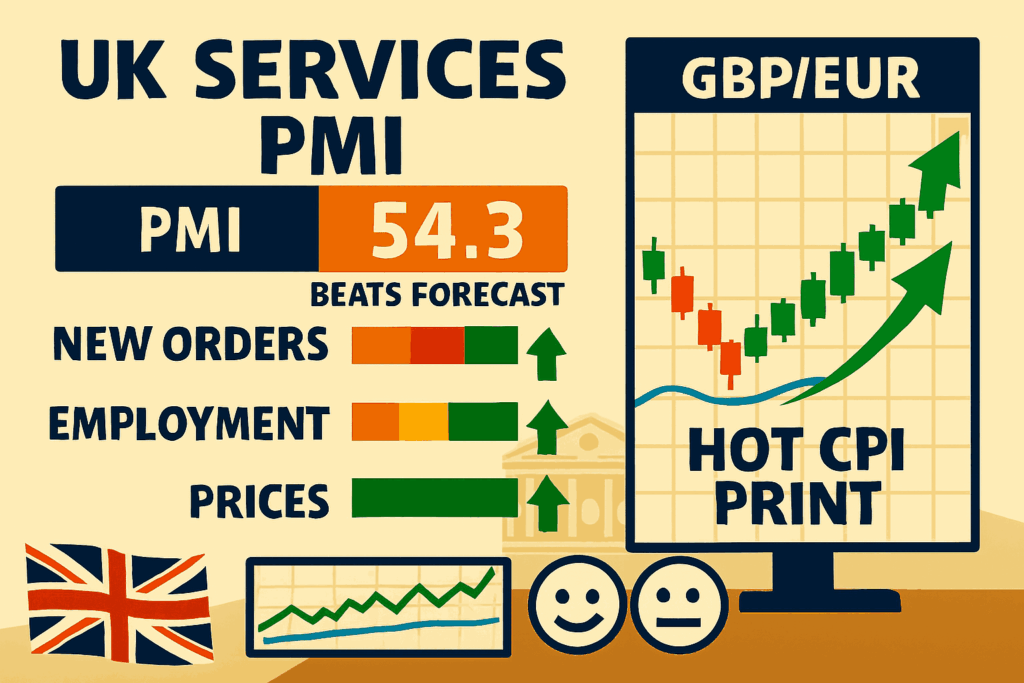

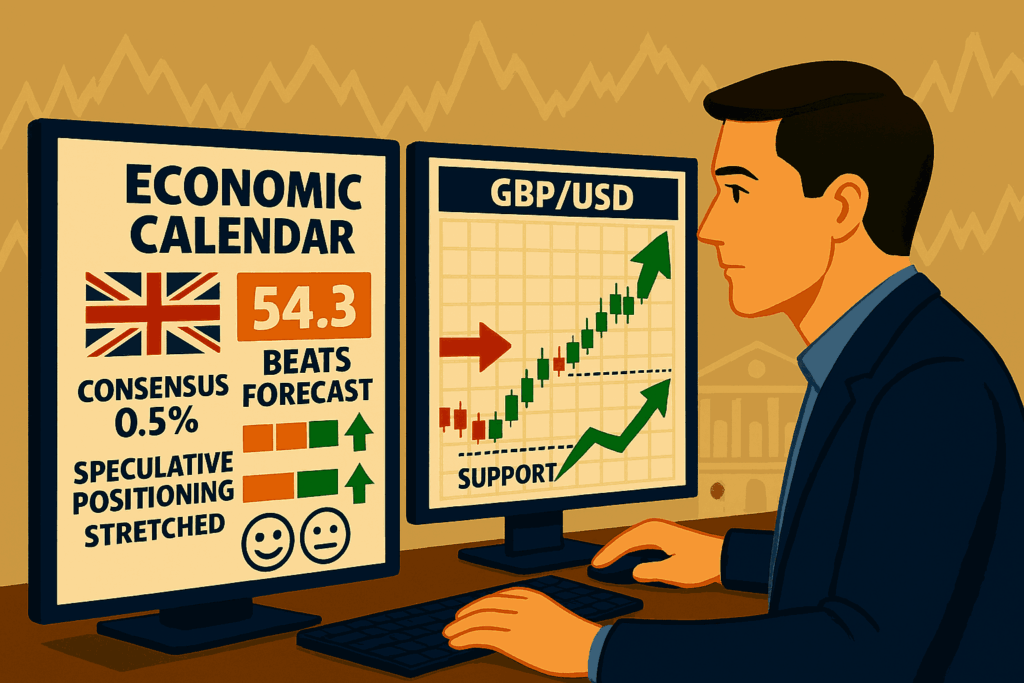

PMI: Early, Frequent, and Sentiment-Rich

PMIs (Manufacturing, Services, Composite) are forward-looking and arrive early each month, giving the first read on growth momentum. For GBP:

- Services PMI matters most (UK is services-heavy).

- New orders, employment, and prices sub-indices hint at future inflation and hiring.

- A strong Services PMI can boost GBP by implying resilient activity and persistent price pressure; weak PMIs flag slowdown risk.

Trading note: PMIs often front-run revisions to growth and inflation expectations, so sterling can trend on a series of beats or misses.

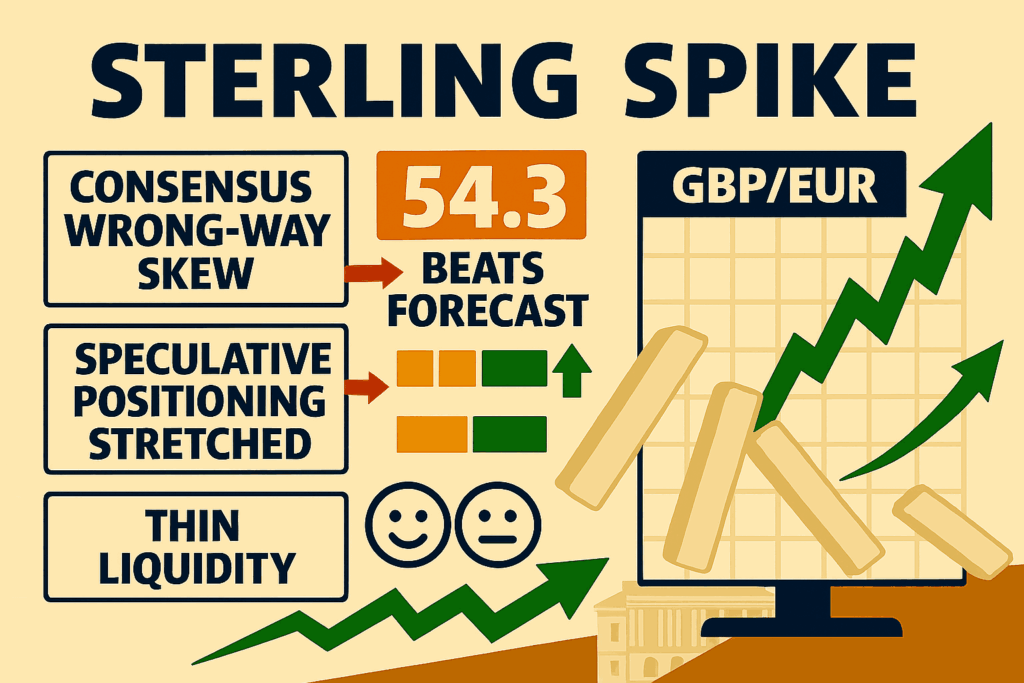

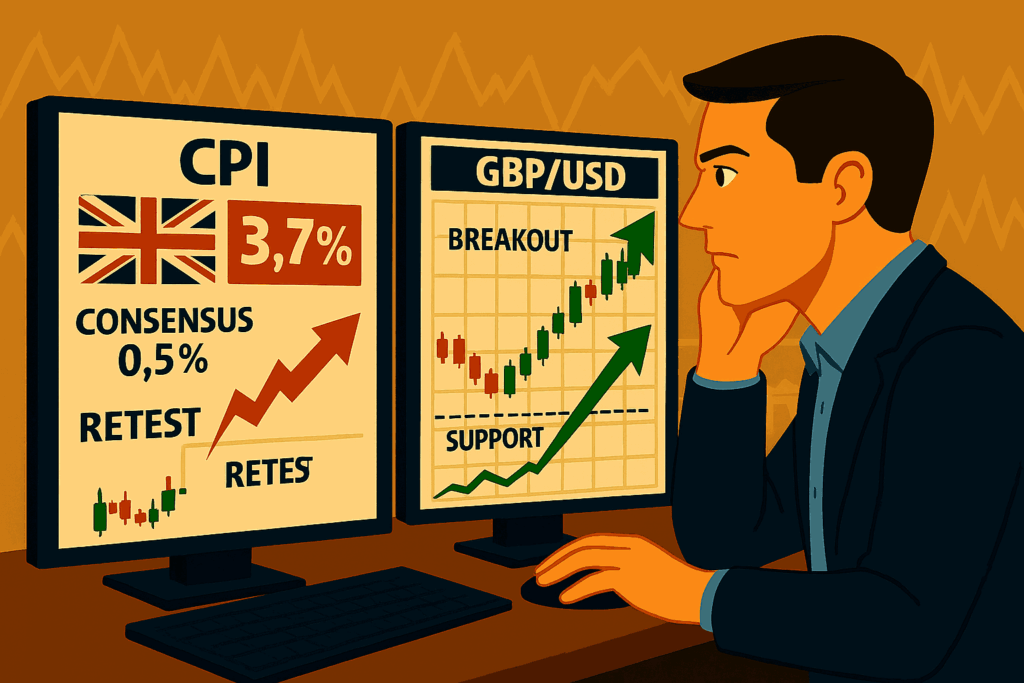

The Surprise Mechanism: Why Some Prints Explode

Sterling’s biggest bursts happen when three forces align:

- Consensus skew: The street is leaning one way; the data flips it.

- Positioning: Speculative positioning (e.g., COT) is stretched, amplifying stops.

- Liquidity: Thin books at release time magnify the first wave.

When a surprise hits, rate-differential pairs respond fastest: GBP/USD jumps when US side is quiet; GBP/EUR reacts when ECB pricing is stable; GBP/JPY is the pure “risk + rates” expression.

A Playbook for CPI/PMI Days

Pre-release (T–24h to T–1h)

- Map consensus and ranges; note whisper numbers.

- Mark levels: prior day high/low, weekly VWAP, supply/demand zones.

- Right-size risk (cut size, widen stops modestly) and avoid pre-positioning unless the edge is clear.

At release (T–0 to T+5m)

- Read headline + core (for CPI) or Services PMI + prices.

- Watch gilt yields and OIS (implied BoE path). If front-end yields surge with a hot print, GBP impulse is more credible.

- Execution: consider stop entries above/below pre-marked levels rather than chasing mid-spike.

Post-release (T+5m to T+60m)

- Expect a fade attempt. If yields and OIS hold the move, buy dips in an upsurprise; sell bounces in a downsurprise.

- Avoid counter-trend trades until the first pullback holds or fails at a clear level.

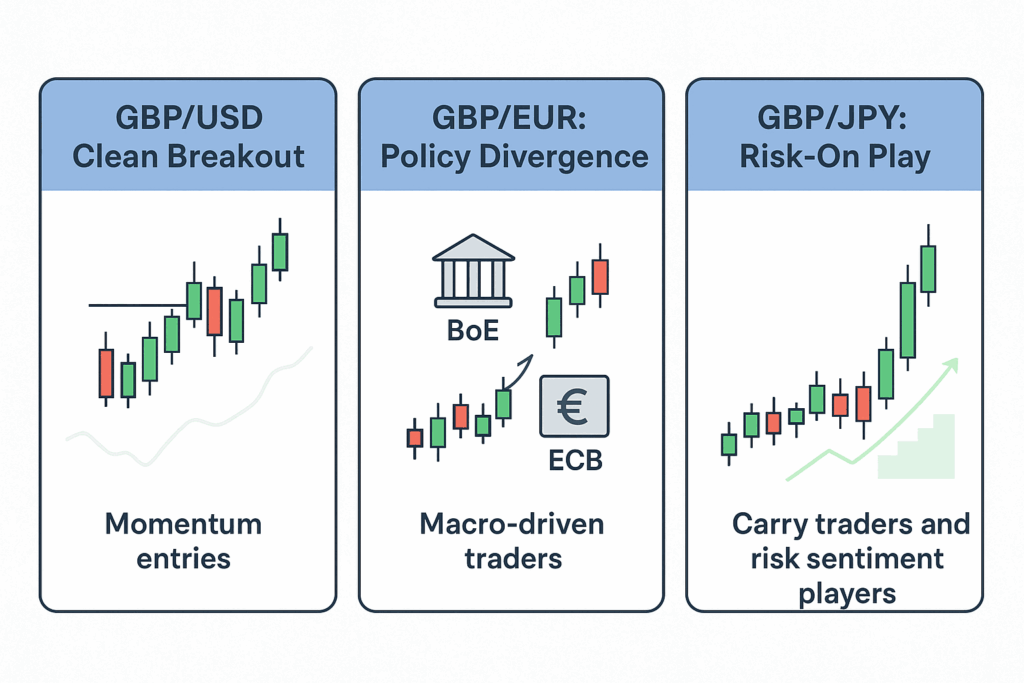

Pair Selection: Express the Right Theme

- GBP/USD: Best when the story is UK-centric and the US calendar is light.

- GBP/EUR: Use when the move is about BoE vs ECB divergence.

- GBP/JPY: Highest beta great for momentum if risk sentiment isn’t deteriorating.

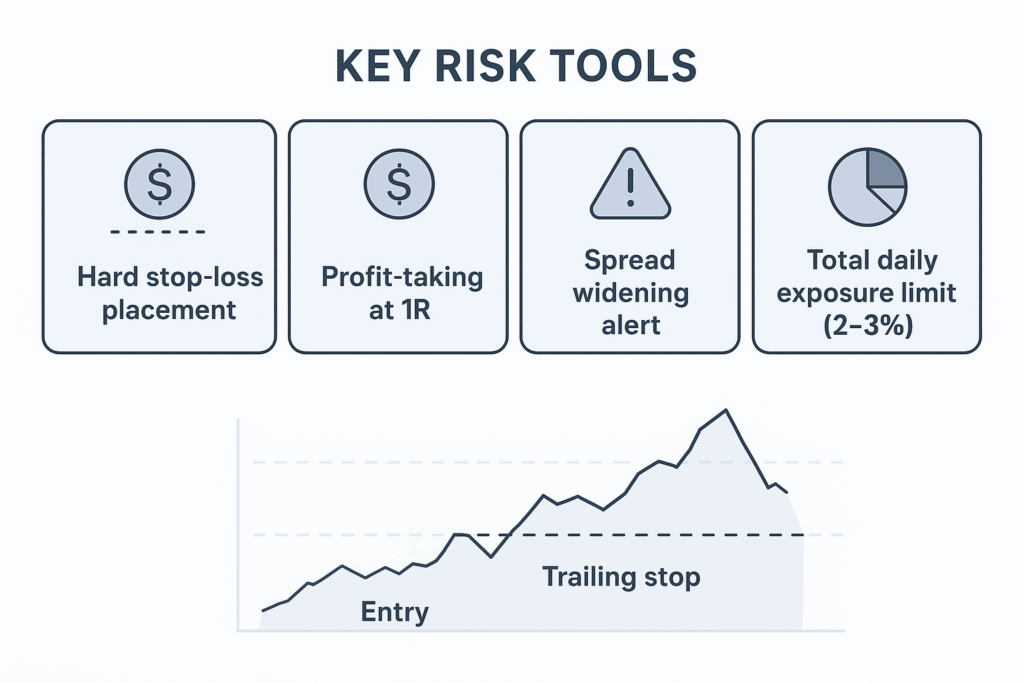

Risk Controls for Volatile Prints

- Use hard stops (slippage happens accept it).

- Consider partial profit at 1R, trail the rest behind structure.

- Beware widened spreads on the first tick; avoid market orders in illiquid seconds.

- Cap total event risk (e.g., max 2–3% across all GBP positions for the day).

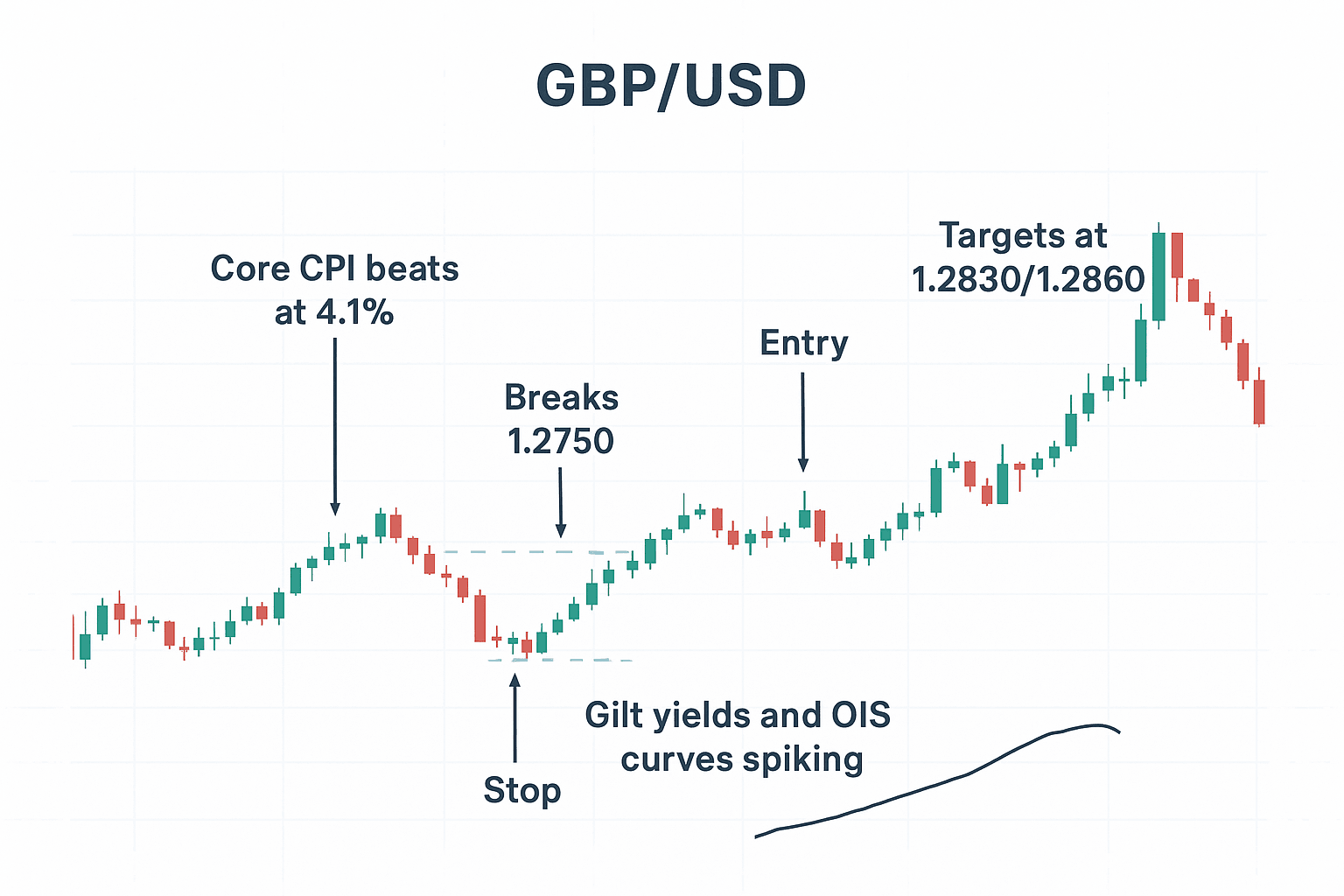

Example Scenario

Consensus looks for Core CPI 3.8% YoY; it prints 4.1% with firm services inflation. Front-end gilt yields jump; OIS adds +15–20 bps for the next BoE meeting. GBP/USD rips through a prior supply at 1.2750. The plan: wait for a pullback to 1.2750–1.2760, place a tight stop below the breakout base, target 1.2830/1.2860 where daily resistance sits. If yields fade, scale out early.

Bottom Line

Sterling spikes around CPI and PMI are about surprise vs expectations, policy repricing, and positioning. Build a repeatable routine: prepare levels, read the right sub-indices, confirm with rates, and execute with strict risk rules. That’s how you convert data shocks into durable GBP edges.